Dateline:Outta Gas and Outta Patience

Dateline:Outta Gas and Outta Patience

Mexico suddenly finds itself in dire straits. A number of things which were neither foreseen nor planned-for have suddenly occurred. Three years ago, sub-$100 oil seemed like an impossible fantasy, at least for consumers. A slowdown or reversal of globalization was seen by no one until quite recently, when Brexit shook the establishment. Trump was considered a long-shot candidate right up to the eve of the election. Worse, the peso has lost nearly 50% of its value over the last two years, recently exacerbated by the Trump victory. And the final blow, gasoline, which remains in plentiful supply on global markets, is now having trouble finding its way to Pemex stations across the country, even at newly elevated prices, which should theoretically stimulate supply.

Of course, the most pressing of these issues is gasoline. Even back in 2014 when I did my road trip, gasoline was a contentious topic in Mexico, having seen a steady upward climb in prices. Now it’s everything. Given the recent, hefty, and indeed record-setting price hike in Mexico, combined with shortage, I decided to do some research to better understand the facts. I looked at DOE data on global production and pricing of crude, and domestic pricing of gasoline. I looked at historical Mexican gasoline prices, and I looked at the exchange rate. I even read through bits of Pemex’s 2015 annual report. I’ve also read many articles in the Mexican press about the situation.

I learned some interesting things. First, since 2010, the price of Magna (regular unleaded) has had one very minor dip (Jan 2016) in an otherwise uninterrupted rise. Mostly those rises have been around 1% per month. Sure, they add up over time, but any given monthly hike is not too big, so people grumble, but then move on.

Relentless Price Increases in Pesos

However, the most recent hike was the biggest ever, 14% in a month for Magna, more for premium. That, along with shortage, has unleashed the simmering fury.

Poor Policy Making in Action

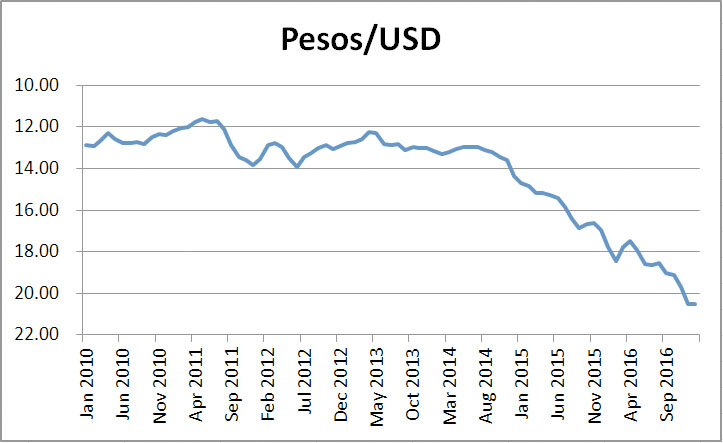

But the real culprit is not gasoline; it’s the USD/MXN (peso) exchange rate. Over a very long time frame, the peso has mostly only moved in one direction versus the US dollar: down. Sure, it’s not a perfectly smooth downward path, but the longer term trend is about as inexorable as any seen in finance. Historically it’s been a mostly gentle depreciation, with a few twists and lurches along the way. More importantly, it’s been manageable both for the economy and for Pemex.

One Direction: It’s Not Just a Boy Band. Pesos per USD Over Time

But things changed in the fall of 2014, when crude oil started to tumble in earnest and OPEC gave up trying to stop it. Suddenly the peso’s gentle, long-term swoon turned into a dive, creating a host of problems, particularly for energy and imported goods.

Gentle Peso Decline Turns into a Swan Dive. Source: Federal Reserve

Not only do currency traders view Mexico’s economy as dependent on oil, and thus vulnerable, but the picture for Mexican oil continues to worsen, well beyond the price of crude. In 2014, along with the global crude price, Mexico’s crude production began to decline at an accelerating rate. Add to this the fact that as the most liquid emerging market currency the Peso gets used as a proxy to short oil, and you have a pile-on to the poor Mexican peso.

Production Continues to Decline, Now at a Faster Pace. Source:DOE

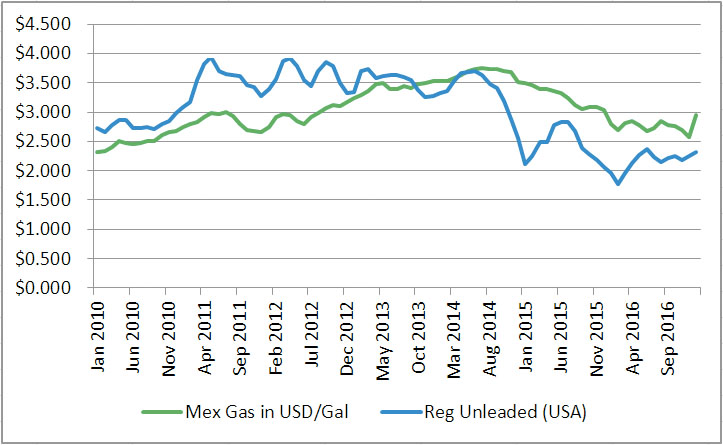

So the gasoline problem is really an exchange rate problem, exacerbated by political bungling, and crippled, inefficient Pemex. In USD terms, the price of gasoline in Mexico has fallen since 2014, which reflects the global reality of excess supply against relatively fixed demand. And prior to late 2013, gasoline was actually cheaper in Mexico than in the USA. Even now, the Mexican price premium is nothing compared to places like Europe or Japan.

US vs Mexican Gas Prices. Converted to USD/Gal at Avg Monthly Foreign Exchange Rate

As for political bungling, Peña Nieto hasn’t helped his own cause. During his 2012 campaign, he promised that the energy reform would spur foreign investment and lower the price of gasoline to consumers. Had he been able to wave a magic wand and immediately turn the creaky Pemex-controlled monopoly into a thriving, competitive marketplace, this might have come true. But given the reality of a very long lead time to that promise, it was nearly impossible that it would work out as expected. In order for him to have been correct, he would need to accurately forecast both the peso exchange rate and the price of crude more than three years out, an impossible task for anyone. Sure, he was correct in essentially saying that Pemex was wildly inefficient. But he erred in thinking he could foresee future prices.

So instead of what he might have expected — a soft decline in the peso, and crude oil trading around $100/BBL — he got a collapse in both, exacerbated by steep production declines at Pemex. Worse, Pemex’s finances collapsed along with the crude price, thus cutting off a source of financing for the Mexican government. So by the time the Energy Reform was passed, and Mexico held its first auctions for oil drilling rights, the big, global energy producers responded with a collective yawn. Most of the drilling rights went unsold, leaving yet another hole in government finances. The majority of Mexico’s crude lies offshore, and it’s expensive to find and expensive to extract. Below $50/BBL it probably isn’t worth the hassle, especially when fracking costs onshore in Texas continue to plummet. Add to that the political risk of operating in Mexico, where the rule of law can be a variable thing, and a weak and bureaucratic justice system operates at glacial speed, and foreign oil producers stayed away.

As for Pemex, it is rapidly on its way to becoming a national liability instead of a national asset. It’s suffering perhaps the worst possible business nightmare of rapidly falling production, and a steep fall in the prices it can charge. Add to that enormous liabilities in the form of pensions and union contracts, and it’s in a tough spot. Oh, and the drug cartels have expanded into pipeline theft, stealing millions of liters of gasoline and disabling pipelines in the process. Add all that together and suddenly you have a state-owned albatross which can only be bailed out by radically higher oil prices, something not on the immediate horizon.

As for the immediate shortage, the above longer-term issues collided shorter-term with the law of supply and demand. While I have zero evidence to support the following thesis, it makes economic sense. Knowing that gasoline prices would be 14% or more higher in January than in December, Pemex and the gas station operators had every incentive in the world to “run out of gas” as December rolled to a close. Right? Hold your gasoline for an extra week or two and suddenly it’s worth 14% more. What sensible capitalist wouldn’t do that? Now, I don’t know if that’s what actually happened, but it seems to be the simplest explanation for sudden shortages around the country. And if that’s correct (and I have to believe it is at least partially correct), then policymakers erred big league in not foreseeing and addressing this problem, possibly via weekly price increases or some other measure.

But whatever caused the shortage, Mexican consumers are now mad as hell, and they feel betrayed once again by a government which is widely seen as rapacious and unresponsive to the needs of the ordinary people. Sadly and ironically, their protests are making things worse. Yesterday I read about a typical Mexican form of protest, shutting down federal highways. While such protests are, in my view, almost always misdirected, in this case they are almost comically misdirected. Not only are hapless drivers now wasting more gasoline idling on stopped freeways, but stalled gasoline trucks can’t make deliveries. Add to that the fact that people are trashing, burning, and sacking those gas stations, and any reasonable observer would conclude that this will only exacerbate the problem.

No Gas? Let’s Steal Toys!

Alas, Mexico is now in a tough spot. There’s zero confidence in the government. People are just angry, and acting out. There are reports now of looting all around the country. Toy stores, electronics stores, and other businesses completely unrelated to gasoline are being looted with abandon. Civic order seems to be breaking down in an unprecedented manner. Given the above, it’s hard to see a rapid resolution to the problem, even at higher prices. Gas stations will take time to rebuild, and as long as the highways remain blocked, gasoline won’t flow. Add to this misery the fact that the peso takes a dive every other time that Donald Trump issues a tweet, and you have a formula for more social unrest. As for the longer-term fallout, no one comes out looking good in this. The government manages to look incompetent, and possibly heavy-handed. The looters look just as bad as looters everywhere, and with handful of deaths to boot, Mexico just got another black eye.

At the root of the problem is the exchange rate as I’ve demonstrated, yet there’s little the government can do, though it is trying. Banxico, Mexico’s central bank, has raised overnight rates five times in 2016, for a total increase of 250 basis points. Each hike put a temporary floor on the peso, but ultimately did nothing to halt its slide. Mexico now has one of the higher overnight rates in the world, which should theoretically attract peso purchases.

But it’s not working. Thursday Banxico intervened directly in the market, purchasing one billion dollars worth of pesos, but the effect lasted all of six hours or so. Friday, Banxico intervened again with another billion.

Market Not Impressed With Banxico Intervention

This time it seems to have halted the slide, at least for now. But such intervention is not sustainable as it will chew up foreign exchange reserves in a hurry. And Mexico’s foreign reserves took a hit in 2015 and haven’t recovered. Moreover, central bank interventions in currency markets have a long and storied history of failure. If the market wants to take the peso lower, it will.

Foreign Exchange Reserves Off Their Highs

So Mexico finds itself in a tough spot. Though the peso could bounce a bit from here in the short term given the recent bolus of bad news, I suspect that it will find lower levels before stabilizing. Trump indeed will build the wall. Though that shouldn’t affect Mexico’s economy directly, it will be a psychological blow for the country and its investors. Worse, Trump has already persuaded several high profile companies not to invest in Mexico. And whether he can actually carry through with his threats or not, we can be certain that any company which had been considering inbound investment in Mexico has to at the very least be delaying such plans to see what comes after the inauguration.

As for this gringo, I’m fairly convinced that now is not the time to be buying property in Mexico. The peso is likely to get cheaper in my view. Between higher interest rates, higher gasoline prices, likely increases in inflation, and a “Trump-nado” about to be released, Mexico is probably looking at a recession in the next year. Given the social fragility that this episode has revealed, one can only wonder what might occur during a full-fledged recession. Buckle up. It’s going to be a bumpy ride.

P.S. This post has been a couple days in the making. This morning’s news suggests that the worst of the rioting and shortages may be over or on the mend. Nonetheless, I believe my conclusion still stands.

P.P.S. For an earlier analysis of the Mexican Peso I wrote in January 2016, click here.

Thoughtful, interesting and well-written article… thanks!

LikeLike

Hola Franz,

Thanks! Should you comment in the future, your comment will be automatically approved. Saludos!

LikeLike

Hello, Kim, it’s late and I should be in bed now but I just needed to read all the interesting comments that your great piece of writing has attracted. The analysis and the data in your post are definitely enlightening, and in these times of turmoil I just wish more Mexicans could be able to read it because many, many people just don’t know what’s going on. I’ll certainly share it around with friends who can read in English. The contributions from your readers are all worth-reading too, their opinions vary so much and I think that’s exactly what makes this post all the more interesting.

Sadly, there was an episode of looting in Monterrey, which is something totally unheard of here, and I sincerely think that nothing of the sort will happen again. The incident happened in an area which is already precarious and affected with various social problems. Riots, burglaries, and violence in general is unfortunately not uncommon there.

I think that we were all enraged when the rise in the gasoline prices were announced, we’ve somehow put up with the slight monthly increases, but a 14% increase is such a blow that many of us felt that it had been enough of turning the other cheek and it was time to throw blows too. We’d like to have answers, but the politicians have been such liars that we just don’t believe them anymore. I’ve read what Peña Nieto has tried to explain and I think he’s not completely wrong, but most Mexicans just don’t believe a word he says and many, many more are dissatisfied with his reforms. And about the gasoline shortage, you’re right! No one believed that we were running out of gas, because hiding merchandise just right before a price rise is a very common practice in Mexico that I’ve seen many times in my life: sugar, toothpaste, cooking oil, etc. Supermarket owners were always to blame, but now it was PEMEX and that we just couldn’t bear… we felt like we were being laughed at.

I totally agree with Chris about the final demise of the Mexican Revolution. Things will definitely be different from now on, and we better find new ways to survive. I think the real Mexican Revolution is just about to begin, ¡que Dios nos agarre confesados! Which is “Lord have mercy”, sort of. Un abrazo, mi amigo… don’t think too much about the property, is it because you want to wait for the prices to go even lower or because you’re afraid of turmoil? Remember that we’re used to fall down and get up again, so there’s Mexico for years and years to come…

LikeLike

Hola Tino,

Thanks for the terrific and thoughtful comment. Though the gasoline price rise is mostly due to the foreign exchange rate and thus out of the hands of the gov’t, I can totally get that people are frustrated and desperate about the dramatic rise of a commodity so essential to daily life. I definitely feel for the Mexican people, many of whom don’t have the extra pesos they’ll be needing. As for trust in EPN, trust in governments around the world seems to be at a record low. After behaving like “rateros” for so long, it’s finally coming home to roost. I think that’s a big driver behind the Trump phenomenon here as folks are sick of corruption as usual. As for me buying property, I’m waiting because I think that prices are likely to decline due to higher interest rates, a slowing economy, and a likely continued fall in the peso. I read this morning that Trump’s administration plans to notify both Canada and Mexico that it wishes to open renegotations of NAFTA shortly after the new administration takes office. That can’t be good for the peso, nor can the construction of the wall, though I think that’s more of a psychological issue than a real one for the Mexican economy. There’s also the matter of a possible bankruptcy of Pemex and the shaky finances of the gov’t too. Oh, and the top Mexican companies all have material USD debts that are getting harder to service every day. In short, there are a LOT of headwinds out there. I’m hoping for the best, but realistically, Mexico faces a host of challenges leading up to the 2018 elections. Buckle up, it’s going to be a bumpy ride. Saludos y un abrazo.

LikeLike

P.S. The IMF just lowered its 2017 growth estimate for Mexico.

LikeLike

It will be a bumpy ride, indeed.

LikeLike

Frankly, there are a lot of financial problems all over the world, including in the USA. Some day it’s all going to blow; only question is when.

LikeLike

Thank you Kim. I was going to attempt a post about the hike in gas prices but I’m glad you beat me to it since you have a better grasp of the data than I do. Even yesterday we found a couple of gas stations in Queretaro that supposedly had run out of gas. Before the New Year, there were lines of drivers at the stations in San Miguel topping off their jalopies’ gas tanks and filling plastic jugs. That struck me not only as futile but also indicative that the people who are going to get most screwed by the price increase are the poor.

Despite the external issues of the decline peso, Trump etc it would seem that the fundamental problem is that the Pemex model—using a totally corrupt, inefficient, cash-strapped operation to plug holes in federal budgets—is totally screwy. It’s a form of indirect taxation, and very regressive taxation at that.

I’m not really clear about Peña Nieto’s energy reform scheme and it’s going to solve any of these problems in the short term, if ever.

Argh.

Al

LikeLike

Hola Al,

Thanks for the kind comment. I totally agree with you about Pemex. I’m still scanning Pemex’s financials, and was surprised to find in their 2015 annual report a “going concern” qualification from the auditors. In short, that means the auditors think Pemex is on the verge of bankruptcy. That surprised me, not that they were in such bad shape, but that they were in such bad shape that the auditors had to put that concern into their report. Mark my words: before this is all through, the general (read poorer) taxpayer is going to be paying for Pemex pensioners’ (richer) pensions. Or, put otherwise, it’s “SNAFU” or “FUBAR.” Saludos and thanks for stopping by.

LikeLike

In the end, this had to happen. As in all countries, those families with low and single incomes always suffer more.

I can’t think of any other way out of the abyss. Suggestions? Let’s hope that the fluctuating prices do go up and down like Canada and the U.S.

As I stated in an earlier post, in many countries people work two jobs, go to school and manage a family all at the same time. I did it, many who read this probably did it. So, as much as we love the laid-back lifestyle of Mexicans, it’s definitely changing.

LikeLike

Hola Chris,

Here’s my suggestion: massively change the laws on petroleum in Mexico. Make the oil the property of the landholder like we have in the USA. But implement a wellhead tax so that the gov’t gets a cut. Break up Pemex and privatize it. There are already parts that are saleable like the retail arm, the chemical biz, etc. Explain to the retirees that there’s no way they are going to get everything they’ve been promised. Perhaps banning public-sector unions first would be the way to go. Invite US frackers into Mexico to get production moving again.

None of these things would be a magic wand, nor would they do anything about the relatively low price of petroleum these days. (And OPEC looks to be fraying once again.) But it would solve a BIG problem, and also reduce the govt’s opportunities to use Pemex for political patronage, a very good thing too.

Now, I know enough about Mexican politics to know the above won’t happen. But it would work if the political will were there.

Saludos and thanks for your contributions to the discussion.

LikeLike

Great article and well researched.. However I don’t think your data supports your proposition that the declining peso caused the increase in gas prices. Please give this some thought in your analysis, although it may be a chicken and egg argument.. The government did not subsidize the price of gas so much as the price of gas and oil subsidized the government. Up until about two years ago, revenue from the international sale of oil provided the government with approximately 38% of its budget. With the falling price of oil and the decline in production, government revenue fell. The government did not raise the price of gas sufficiently to compensate for the falling revenue. In order to maintain infrastructure programs the government increased the national debt hoping for a recovery. Oil prices and production continued to decline and debt increased without a reduction in infrastructure expenditures. As a result the peso began a drastic decline. A collapse of the peso would result in the collapse of the Mexican economy. A reduction in infrastructure would result in a collapse of the government. An increase in gas prices could be tolerated and EPN bit the bullet.. It seems the cause lies more with the falling price of oil and the government reliance on the finite resources of oil and debt to maintain infrastructure.

EPN’s speech of December 21, 2016 seems to confirm this explanation. Calderon’s response is also apropos. Calderon stated that if Trump continues to hammer away at the Mexican economy, by deterring investment in Mexico, he is in store for a real immigration problem.

LikeLike

Hola Carlos:

Interesting points all. Clearly the Mexican federal budget is closely intertwined with the health of Pemex which of course depends on production volumes and the price of oil. As you point out, Mexico has multiple, hard-to-solve problems. But it’s also hard to argue that, absent subsidies, there was any other route than higher for gasoline prices in pesos, given the swoon the peso has suffered. That said, thanks for the additional detail. Future comments will be immediately posted. Saludos!

LikeLike

Back again after commenting on your Dec 31post. After reading the content of “Mexico is Burning” , I am not surprised, but I am so incredibly sad.

I also commented today on my blog about the situation. The only resource that this government hasn’t completely depleted is the people. In other dire times, they have proven that they are “milagro mexicano”. We have to take a deep breath and see what happens next, with this Kafka-like situation.

LikeLike

Hola Joanna,

I feel pretty much the way you do: sad, but not surprised. Well, OK, maybe a little surprised at all the looting. I don’t recall such a thing ever having happened in Mexico, nor does Luis. Let’s hope it doesn’t start a trend. Such behavior is already enough of a problem NOB. And yes, I agree with your oberservation of the Mexican people who seem incredibly resourceful in the face of constant obstacles. May god bless them with a much better government some day. Saludos y un gran abrazo.

LikeLike

Yes, God bless us all… we need it

LikeLiked by 1 person

The way I see it:

While the know it alls were propounding the myth of peak oil, the oil men were developing deep drilling, lateral drilling and fracking technology. And now, we have the miracle of shale oil.

The Saudis saw a threat to their one product ecomomy. They financed a propaganda campaign against fracking, but it didn’t work. Those shale deposits ocurr all around the world. It was impossible to put a lid on it.

They then began dumping the product hoping to price shale oil out of business. It darn near worked. US oil and gas firms went into bankruptcy so fast, I quit counting them. Leasing dried up, but production continued.

The Saudis had created a welfare society dependent upon the petroleum industry. People lived good because they were dependent upon government employment or some other sinecure.

Rather than invest their income in a diversified economy, the Saudis financed religious schools. They could tell you all about the Koran and the Hadiths, but it took a couple of Pinoys to change a tire.

Saudis didn’t work. Imported labor did.

Sadly, it seems that people will not accept that they must live a lower standard of living. If the government cannot or will not fund the social welfare state, the alternative seems to be ISIS.

Just as the Saudis began running defecits, someone in Washington decided to let the Iranis out of their carefully crafted box of sanctions. Irani oil was on the market.

Worse, Irani funds and assets that had been seized were returned.

Sometimes bad things happen to good people. Nations that were heavily dependent upon petroleum income suffered. Russia, Nigeria, Venezuela and Mexico were in trouble.

The miracle of fiat currency allows governments to solve their problems with the printing press. This produces inflation and robs the people of their savings. Soon we all will be living in a Zimbabwe world.

The era of the Petrodollar is ending.

LikeLike

Hola Robert,

Lots of interesting points in your comment. Thank you! Saludos!

LikeLike

On Thursday I drove 9 hours from central Mexico to the Pacific. No rioting, no shut down stations no fires. Little traffic – fuel plentiful. Luckily,Mexico’s #1 revenue generator is remittances from the USA………..not gasoline.

LikeLike

Hola Barbara,

I’m glad you were finally able to make your trip, and peacefully to boot. Happy vacation from the never-ending drudgery of retirement in San Miguel de Allende. 😉 Saludos and thanks for stopping by!

LikeLike

My, that was quite a post, and you didn’t earn a penny for it.

As for there being “zero” faith in the government, that might be the appearance for someone not living here. Actually, the government at all levels does quite a few things quite well. And some things quite poorly. This gasoline issue, for instance.

LikeLike

Hola Felipe! Muchas gracias. Do you know any Mexicans with much faith in their government? I don’t. Saludos!

LikeLike

Great business article. So your real estate purchase is on hold till the oil slick settles?

LikeLike

Hola Patz! I’m still fantasizing about my penthouse, which remains on the market. Obviously it keeps getting cheaper and cheaper. But given all that’s going on, there’s a decent chance of recession, which should create some deals in real estate. And much higher interest rates, which Mexico already has, should also do the same. So time is on my side, at least for now. Saludos and thanks for stopping by!

LikeLike

I think it’s not a matter of concern. It is actually a matter of a very positive change, a new wind over Mexico. The Mexican Revolution was a disaster which led Mexico into a never ending abyss over a period of 85 years. It’s slow but eminent demise has finally come. The nationalization of petroleum, banks, and other corporations along with the union or monster Pemex created destroyed the opportunity for Mexicans to truly shine.

We now join the ranks of other great world economies. Change is here and not all Mexicans are prepared for it. What will actually happen is that gasoline, like in every other modern and industrialized nation, will now fluctuate in price. This is a severe lesson in growing pains. We will suffer in the beginning but will find our place in world markets in the next three years.

You will begin to see some wonderful changes once things have settled down. I can understand your concerns but it’s nothing like you have written. This is the final chapter in the Mexican Revolution and why it was doomed to fail from the beginning. Another good case study is Venezuela. Unfortunately, Venezuela didn’t or could’t accept the tides of change and has now run itself into the ground.

Good for Mexico that we have been on a steady course to this change in the economy. Fuel prices will begin to fluctuate just as in any other country as of February 18th. Prices could go up or down and it is based on, according to the assistant secretary of energy Miguel Machmesser, the price of oil and the dollar/peso exchange.

The next year won’t be easy but companies like FEMSA, the owner of OXXO convenience stores, 7-Elevens, Extra, and oil companies such as Exxon, Chevron and Shell, would not have invested so heavily in gas stations and convenience stores if they thought this was the end. So just like stations in the U.S. that make pennies on a gallon of gas but lure customers into their convenience stores, Mexico will do the same.

At your local OXXO you can now make bank deposits, credit card payments, purchase travel car insurance, bus tickets, make payments for MercadoLibre (Mexican Ebay), pay bills, purchase air time, send money to anyone in less than ten minutes from any place in the world, and the list goes on. This has all been carefully worked out.

Mexico has come of age. I for one am very excited about it and feel that my future is now more secure in Mexico.

LikeLiked by 2 people

Hola Chris,

I share your enthusiasm for free markets and non-government players. But did you read the whole post? The sole reason gasoline hasn’t fluctuated down since it started declining in the USA is solely due to the exchange rate. And that is something the government can’t much influence. And even in a free market, if the exchange rate declines enough, then expect to pay more for internationally traded goods. That’s what’s happening in Mexico. Yes, the Jan 2017 price increase was big, but the peso declined 3.3% in December, while US gasoline is up 16%. There’s your increase for January. Doesn’t look free market yet, but the free market would have produced about the same result, albeit more smoothly and without the shortages. Saludos and thanks for commenting.

LikeLike

P.S. What’s of concern is not the freeing of the market, but the decline in Mexican living standards due to the exchange rate, and also the rioting/looting that occurred as a result.

LikeLike

The rioting and looting is less than you might think, and it’s winding down. Oddly, my normally turbulent state of Michoacán did not participate.

LikeLike

Yes, as I wrote in my PS, the worst seems to have passed. And all those creaky pipelines, old trucks, etc. seem to have gotten to the gas stations. This only supports my idea that gasoline suppliers were simply holding out for higher prices. And once again, human nature reveals itself for what it does, not for what people want it to do.

LikeLike

The deregulating has not had much of a chance to bear fruit. It’s way too soon. The big import depot being planned over in Progreso is still nothing but prints. Horizontal drilling on old fields that were considered depleted using the old methods of production will be exploited even at 50USD per barrel. It is just going to take a little time. A well done essay Kim, I enjoyed it. I was pestering Steve Cotton about gas pricing just a few days ago, trying to get a handle on what is going on in the Mexican gas market.

LikeLike

Hola Norm!

I’m glad you liked the analysis. I agree, the reforms haven’t had much time to work. But as the piece indicates, gasoline prices aren’t all that far out of whack in USD. It’s just the exchange rate has impoverished Mexicans more than they previously realized. And I think Peña Nieto has been unwise to not point out the fx roots to the problem. As for what will happen, Pemex is teetering financially. Something’s going to have to give, and if it’s Pemex pensions, well, there could be a lot more upheaval in the future. Saludos and thanks for your comment.

LikeLike

This will take a year to a year and a half to play out. My college age nieces and nephews ask me what I propose. I told them frankly, get off your duffs, get a job and continue studying. In the U.S., Canada and many other countries, people work two jobs, some people work seven days a week to make ends meet. We’ve had it all to good here in Mexico and LA for too many years living on low prices and government subsidies. We’ve created most of this mess ourselves. I told them to gear up and get ready for the future. It won’t be studying to secondary and then working in a factory for 1000 pesos a week plus all the benefits. Those union days are going going gone. Don’t rely on your government, your pension, your social security, nothing. Make yourself independent. BTW, I’m not getting comment post alerts to my email.

LikeLike

Hola Chris, I think you gave your nieces and nephews good advice, and a pretty clear (and likely accurate) view of the future. Automation is taking the jobs of even the cheapest laborers, so the only defense is to learn something machines can’t do, even if it’s something as simple as cutting hair. As for the email response, there’s really nothing I can do about that, though I’ll double check. You’re sure you’ve used the right email address and clicked all the proper links? In any case, thanks for your contributions to the discussion. Saludos y buen día!

LikeLike

Thank you, Kim, for your thoughts and analysis. Who knew that compressed dead dinosaurs and a Loompa-Loompa wearing a golden squirrel could cause such pain throughout North America. I believe that Canada is in for a further decline, as well.

LikeLike

Hola Debora,

Whether we like it or not, petroleum and its distillates are the world’s most important commodity. Wars have and will be fought over it. And it’s crucial to current lifestyles. Thanks for your comment. Saludos!

LikeLike

Kim, I’m a longtime lurker; yours is one of my favorite blogs. I appreciate your perspective on Mexico’s gas prices and how they are affecting the Mexican economy. Thanks!

LikeLike

Hola Neil! Thanks for coming out of the shadows. I truly appreciate your comment. Don’t be shy in the future. Saludos and thanks for stopping by. Future comments will go straight through, provided you use the same username and email.

LikeLike